The U.S. housing market faces historical challenges. Experts state that Americans are struggling to become homeowners due to the gap between wages and rising home prices. Data from JP Morgan reveal home prices grew by 60% since COVID-19. Mortgage rates are higher than usual, a trend since 2022. Census data report a homeownership rate of 65% last year, the lowest since 2019.

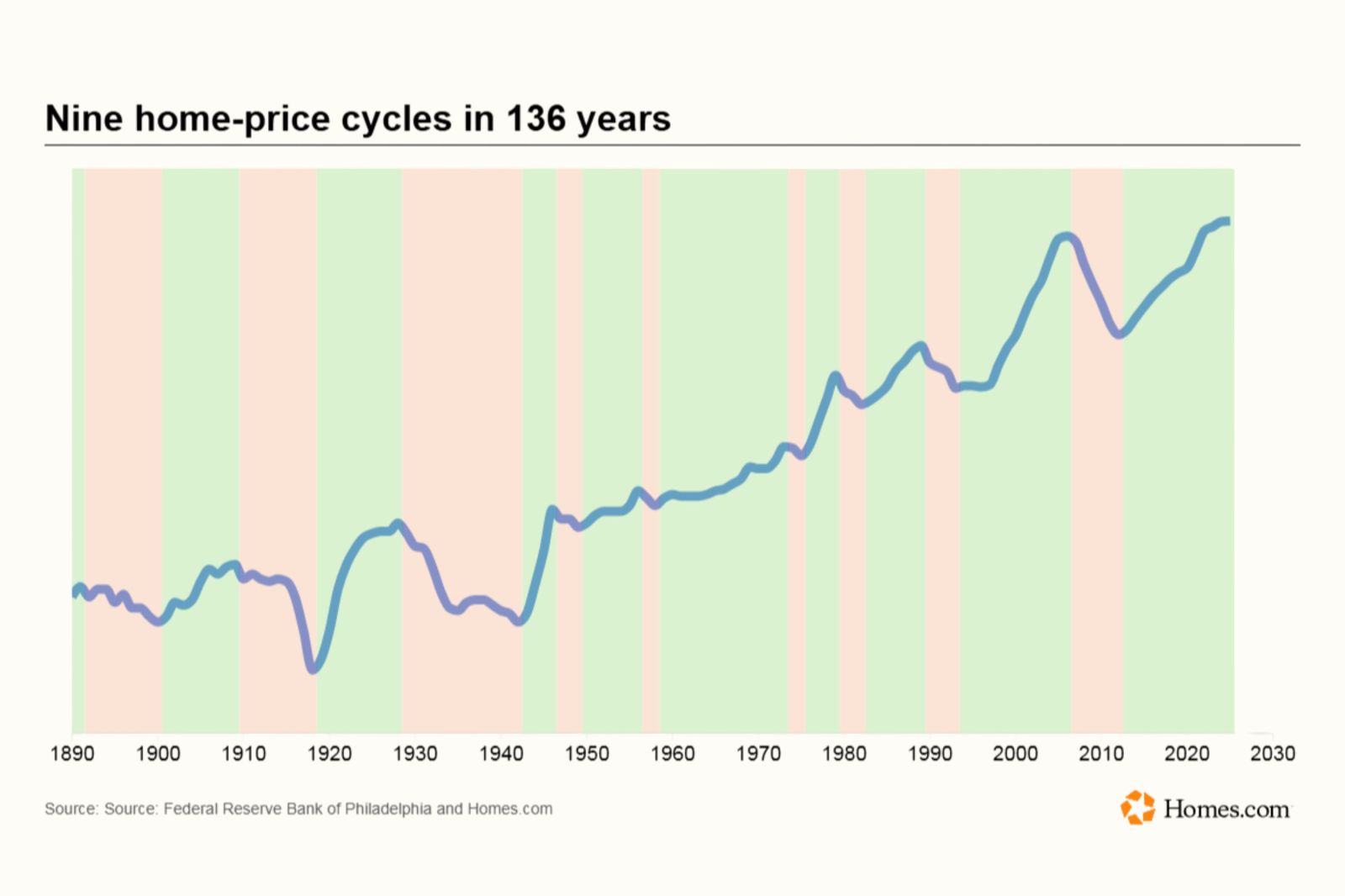

We have the highest home prices on record, along with high mortgage rates. The mortgage rates aren’t the highest on record—they exceeded 18% in 1981—but they are higher than they have been in the last 10 years.

Fairweather emphasizes hard times for those trying to enter the housing market, especially young people. The struggle touches America’s identity centered on property ownership since its founding. The promise of life, liberty, and property shaped the nation, influencing policies.

Historical acts such as the Homestead Act of 1862 encouraged land ownership. The U.S. attracted European immigrants with the opportunity for land ownership, unlike Europe. This ideal has shaped American identity and economy.

Rising Concerns

The housing dream is fragile for many Americans as they face barriers to homeownership. Joel Berner from Realtor.com notes homeownership builds generational wealth. It aligns with American values of independence and self-reliance, being integral to culture and identity.

Fairweather shares a belief about wealth in America. Homeowners often hold wealth, while renters struggle with debt. Policies aimed to convert more people into homeowners in the 1990s and 2000s appeared flawed after the 2007-2008 housing bubble burst.

Despite setbacks, homeownership remains a key American dream. A 2025 Realtor.com survey found two-thirds aimed to own a home.

Challenges of Affordability

Brad Case from Homes.com argues that affordability crises stem from shortages and viewing homes as investments. Historically, fixed-rate mortgages in the 1930s expanded homebuying opportunities.

Recently, rapid price increases have outpaced inflation and incomes. Viewing homes as investments drove higher house prices. Existing homeowners oppose affordable housing construction.

Trump aimed to maintain home values, yet affordable buying remains elusive. The post-pandemic market, with doubled mortgage rates, halted potential buyers.

Fairweather describes a stuck housing market. Homeowners hesitate to move due to low past mortgage rates. Prices remain resistant to change despite higher mortgage rates.

Berner points to structural challenges limiting supply to meet demand. Current efforts focus on reducing regulatory construction barriers.

Future Prospects

Signs of market recalibration exist, although uneven. The Southern and Western markets adjust prices as demand stabilizes. The Northeast and Midwest wrestle with restricted inventory.

Experts predict gradual affordability improvements. Wage growth and stable mortgage rates could aid the situation. Baby boomers may yield homes to younger generations, promising affordability.

Fairweather cautions about future costs. Rising climate-related insurance costs impact affordability. Old homes from retiring baby boomers may require significant maintenance.

Location remains a critical factor. Areas like Florida and Arizona may see affordability changes, but places with job opportunities still demand more housing.

In essence, while affordability could improve, continuous efforts are essential for an equitable housing market.

According to Case, income growth is key to affordability. Addressing the notion of homes as investments might alter perceptions. Ultimately, choosing homes based on preference instead of investment could help stabilize the market.